In

EQUITY SECURITES: COMMON AND PREFERRED SHARES

COMMON SHARES

- Common shareholders are the owners of the company. Therefore, their claims on the company’s revenues and assets are (in the following order) behind:

- Bondholders

- Debenture holders

- Preferred shareholders

- Common shareholders

- Dividend payments are not “guaranteed” in the manner that interest payments are. Dividends are paid at the discretion of the Board of Directors

- Common shares are now registered in street certificates – in the name of the securities dealer rather than the investor. This facilitates easy trading

- Clearing and settlement: CDS Clearing and Depository Services offers computer-based systems to replace certificates

- Trading units: A standard trading unit is usually 100 shares and a group of shares less than that is called an odd lot

BENEFITS – COMMON SHARE OWNERSHIP

- Potential for capital appreciation – for many investors this is the main attraction of common shares. There is the potential for a compounding effect of one’s returns, assuming that the company retains its earnings over time and reinvests them profitably in the business

- Right to receive dividends

- Voting privileges – including ability to elect directors and vote on other important issues affecting the company

- Favourable tax treatment of dividends and capital gains

- Marketability – facilitated through stock exchanges

- Right to receive copies of annual reports and quarterly financial reports

- Right to examine company documents

- Right to attend Annual General Meetings and question management at those meetings

- Limited liability – the most that an investor can lose is his/her original investment in the company

RISKS – COMMON SHARE OWNERSHIP

- The issuer has no obligation to pay dividends

- Common shareholders generally have very little influence over the day-to-day operations of the company

- Common share prices can be volatile, and price changes can lead to investors losing money

- In terms of claims to assets, common shareholders fall behind creditors, bondholders, and preferred shareholders in the case of bankruptcy or dissolution

DIVIDENDS

- A company’s net earnings after payment of preferred dividends belong to the common shareholders. Mature

companies (such as banks) pay a high ratio of their earnings out as dividends; growing companies (technology) typically retain a high proportion of earnings within the company - Most established companies pay a regular dividend, which is usually paid quarterly. In addition, some companies may pay an extra dividend, usually at the end of the Fiscal Year

- When the Board of Directors decides to pay a dividend, the amount, record date and payment date are part of that announcement

EXAMPLE: “The Board of Directors of Canadian National Railway Company has declared a quarterly dividend of $.375 per share on the outstanding common shares. The quarterly dividend is payable on June 30, 2018 to shareholders of record at the close of business on June 9, 2018.” - Dividends may be paid in the form of additional stock rather than cash. Stock dividends are treated as regular cash dividends for tax purposes

DIVIDEND PAYMENT DATE CHRONOLOGY

- There are four important dates in the dividend chronology: cum-dividend date, ex-dividend date, record date and payment date

- The cum-dividend date is always two business days prior to the record date. This is the latest date an investor can purchase the shares and receive the dividend

- The ex-dividend date is the next business day after the cum dividend date. Investors who held the shares on the cum dividend date could sell their shares and still receive that dividend on the payment date. Alternatively, an investor who purchased the shares on the ex-dividend date and held the shares on the payment date, would not receive that dividend

- The record date is important to the extent that with it, investors can determine the cum and ex-dividend dates

- The payment date is the date on which the money is actually received by the investor

VOTING PRIVILEGES

- Not all common shares have voting privileges – or the same voting privileges relative to other common shares

- Restricted shares are common shares that give the shareholder the right to participate to an unlimited degree in

the earnings of the company, but do not have full voting rights. There are three categories of restricted shares:

- Non-voting – have no right to vote, except in limited circumstances

- Subordinate voting – have the right to vote, but another class of shares carry a greater voting right on a per share basis

- Restricted voting – carry a right to vote, subject to a limit or restriction on the number or percentage of shares that may be voted by a person, company or group

- Stock exchanges require that restricted shares are identified by the appropriate term and disclosure documents such as information circulars and annual reports are sent to shareholders describing the restrictions on the voting rights of the restricted shares

STOCK SPLITS AND CONSOLIDATIONS

- Stock splits generally occur when a company’s common shares have been appreciating rapidly in price. The Board of Directors submits a by-law for approval, whereby common shareholders will exchange their current number of shares for a greater number – the typical formula is 2 for 1

- A stock split of 4 – 1 means that an investor will have four times the number of shares at approximately one-quarter the previous price. A stock split should not affect either the value of the investor’s holdings, or his/her proportionate ownership in the company

PRE-SPLIT:

100 shares at $25

POST-SPLIT: 400 shares at $6.25

EXAMPLE: “An investor purchased 500 shares of ABC Company when it IPO’d, paying $30 per share. When the shares reached $45, the company executed a 3 for 1 split. When the shares were $22.50 on a post-split basis, the investor sold 500 shares. What is her profit on this sale?”

To solve this type of question, adjust the original purchase price by the terms of the split: 500 shares at $30 is the equivalent of buying 1,500 shares at $10. Therefore, her profit would be ($22.50 – $10.00) x 500 = $6,250

SPLITS AND CONSOLIDATIONS (cont’d)

- A reverse split or a consolidation has the opposite effect – it means a reduced number of shares at a proportionally higher price per share

- A common motivation for a stock split is to increase the marketability of the common shares, making it more affordable for an investor to purchase one board lot

- A common motivation for a consolidation is to increase the market price of the common shares, allowing them to remain listed on a major exchange such as the TSX or NYSE

READING STOCK QUOTATIONS

52 weeks

| High | Low | Stock | Div. | High | Low | Close | Change | Volume |

| 12.55 | 9.25 | BEC | .50 | 10.65 | 10.25 | 10.35 | +.50 | 6,000 |

- The “High” of 12.55 refers to the highest price the security has traded at over the past 52 weeks

- The “Low” of 9.25 refers to the lowest price the security has traded at over the past 52 weeks

- “BEC” is the trading symbol, or ticker symbol of the stock. This is an abbreviation that traders use when they enter orders for the stock on their computer systems

- “.50” is the annual dividend that BEC has paid over the past 52 weeks

- “10.65” is the highest price BEC traded at in the last day’s session

- “10.25” is the lowest price BEC traded at in the last day’s session

- “10.35” is the last price BEC traded at in the last day’s session

- “+.50” refers to the change in the closing price from the previous day. This means that BEC closed at 9.85 the day before

- “6,000” is the number of BEC shares that changed hands that day

PREFERRED SHARES

- Preferred shares occupy a position between common shareholders and bondholders

- Preferred shares are “preferred” because they receive dividends before common shareholders and have preference with respect to assets upon dissolution of the company

- If a company has a series of preferred shares and they all rank equally with each other, they are described as pari passu

- Companies issue preferred shares because they involve a fixed payment – like debt instruments – without the payments of interest being legally binding

- Investors buy preferred shares because they provide income and the income is tax-advantaged compared to the receipt of interest income

PREFERRED SHARE FEATURES

- Most shares have a cumulative feature. If the company misses a preferred share dividend payment, the unpaid dividends accrue in arrears and must be fully paid out before the common shareholders receive any dividend payment

- Many preferred shares have the callable feature, which is a convenience to the issuer rather than the purchaser

- Preferred shares generally only have voting privileges after a stated number of dividends have been omitted

- Many preferred shares have purchase funds and/or sinking funds. The purchase fund feature is advantageous to the purchaser, acting as a price support

CONVERTIBLE PREFERREDS

- Similar to convertible bonds and debentures in that these securities allow the investor to receive a stipulated number of common shares at predetermined times

- At issue, the conversion price is above the market price of the common – in selecting convertible preferred shares, investors look at the conversion cost premium and payback period to make their decision on which convertible preferred is most favourable

OTHER TYPES OF PREFERRED SHARES

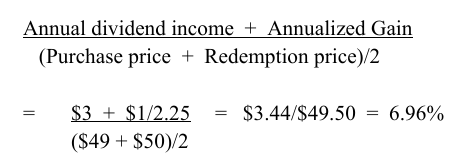

- Retractable preferred shares allow the investor to force a redemption, either in cash or in common shares (in which case it is a soft retractable)

EXAMPLE: An investor purchased a 6%, $50 par value retractable preferred share at $49, retractable at the holder’s option in two years and three months. What is the yield?

- Floating-rate preferreds pay dividends that change with changes in interest rates

- Foreign-pay preferreds pay dividends in a foreign fund – generally American dollars in the Canadian marketplace

- Participating preferreds have rights to a share in the earnings of the company over and above their specified dividend rate

- Deferred preferreds do not pay out a regular dividend. Instead, the shares mature at a preset future date and the return is based on the future price and the redemption value

STOCK INDEXES AND AVERAGES

- Stock indexes and stock averages are used to measure changes in a representative grouping of stocks

- Stock indexes weight the stocks according to their market capitalization. Stock averages weight the stocks according to their market price

EXAMPLE: ABC Company is $20 and there are 10 million shares outstanding. DEF Company is $10 and there are 50 million shares outstanding.

Stock Average: ($20 + $10)/2 = $15

Stock Index: ($20 x 10mil + $10 x 50mil)/60 mil = $11.67 - A stock average gives the heaviest weighting to those shares with the highest market price. A stock index gives the heaviest weight to those shares with the highest market capitalization

CANADIAN MARKET INDEXES

- There are two major indexes calculated in Toronto, the S&P/TSX Composite Index and S&P/TSX 60 Index

- To be included in the S&P/TSX Composite, a stock must meet specific criteria based on price, length of time listed on the exchange, trading volume, capitalization and liquidity

- The S&P/TSX 60 Index comprises the 60 largest companies (by market capitalization) on the TSX. It is divided into 10 sectors, the heaviest weightings belonging to the Financials, Energy and Materials sectors and the lightest weights belonging to Utilities, Health Care, Consumer Staples and Consumer Discretionary

- The S&P/TSX Venture Composite Index is the benchmark for the public venture marketplace

UNITED STATES MARKET INDEXES

- Dow Jones Industrial Average (DJIA) – made up of 30 stocks that trade on the NYSE and Nasdaq. This is an average – or price-weighted – which means that it does not take market capitalization into effect. The DJIA is composed of blue-chip stocks with a lower risk profile than the overall market, hence it tends to under-perform the broader markets in the long run

- S&P 500 – market capitalization weighted, consists of the 500 largest companies that trade in the United States. This has become the main gauge for measuring the investment performance of institutional investments in the United States

- The NYSE Composite Index – includes all listed common equities on the New York Stock Exchange. There are additional indices for industrial, transportation, utility and financial corporations

- NYSE American Index – market weighted index is based on all the stocks listed on the NYSE American exchange. This is a leading exchange for small cap companies

- Nasdaq Composite Index – market capitalization weighted index of more than 4,000 stocks that trade over-the-counter… often used as a proxy for the Tech sector

- Value Line Composite Index – an equal-weighted index of 1,600 stocks, this is the broadest available barometer of all the U. S. indexes, including companies that are listed on the NYSE, NASDAQ, NYSE MKT, and the TSX

INTERNATIONAL MARKET INDEXES

This will likely be tested in the following way: “Investment Advisor John Doe’s client, Jane Smith, believes that Japan’s (or the UK’s or France’s or Germany’s) economy will outperform over the next decade. Therefore, John Doe should overweight Jane Smith in which of the following international indexes or averages?”

- Nikkei Stock Average (225) Price Index – calculated like the Dow Jones Industrial Average, the Nikkei tracks performance in Japan

- FTSE 100 Index – 100 largest listed companies by market capitalization in the United Kingdom

- DAX Performance Index – Germany’s DAX consists of 30 blue-chip stocks

- CAC 40 Index – based on 40 of France’s largest 100 companies, calculated by market capitalization

- Swiss Market Index – Switzerland’s blue-chip index, made up of a maximum of 20 of the largest and most liquid stocks on the Swiss market, ranked by market capitalization

Author

shanghaizhangyijie@gmail.com